News

Sarah's Story

A brief history of how we got here.

When purchasing a property, no one wants any financial surprises. Here we explain Service Charge in as much detail as possible. Including how it is budgeted, paid for, and what to look out for when buying a leasehold property.

A message from the Directors of Cleaver Property Management, following the latest Government update on Covid-19.

After a 40+ year career (more than half of that spent as Director of Cleaver Property Management), Martin Cleaver has retired. Here are his thoughts on retirement, and how the past year has affected his plans.

New guidance regarding EWS1 forms has brought all buildings into scope, what does this mean for your property?

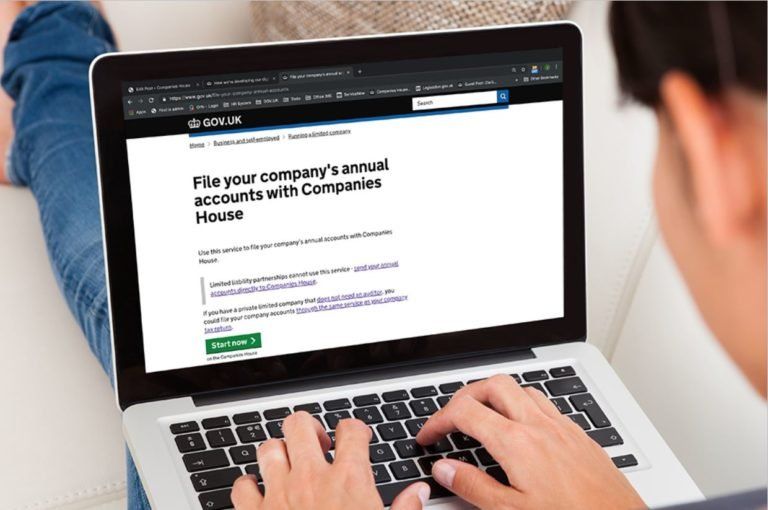

Companies House have launched a free online learning tool to help flat management company directors understand their responsibilities.

From virtual bingo to charity challenges, find out what the Cleaver Property Management team have been up to in lockdown...

The team at Cleaver Property Management got involved with the 2.6 Challenge last weekend. Watch the video and find out how much they raised now...

Advice on how those in communal living can best cope with isolation, through respect and tolerance for your neighbours.

Interested?

Request Our Guide

Whether you’re new to Property Management or looking for a new Managing Agent, your first step should be to download a copy of our report “How to Hire a Property Management Company”. This is an unbiased report advising you of the things to look out for and the questions to ask. Simply fill in this short form.

Alternatively, get in touch on 0118 978 7182

or info@cleaverproperty.co.uk

to discuss your requirements in more detail.

Contact Us

Cleaver Property Management LtdUnit 4, Anvil CourtDenmark StreetWokinghamRG40 2BB

Tel:

(UK)

0118 978 7182

(Overseas)

+44 1189 787 182

Emergency Out of Hours:

0115 896 5158

Email:

info@cleaverproperty.co.uk

We are open 09:00-17:30 Monday to Friday.